How FICO Scores Shape Your Path to Homeownership in Utah

UTAH RESIDENTIAL REAL ESTATE: In Utah’s competitive housing market — from Salt Lake City’s growing neighborhoods to the mountain communities […]

UTAH RESIDENTIAL REAL ESTATE:

In Utah’s competitive housing market — from Salt Lake City’s growing neighborhoods to the mountain communities of Park City and St. George’s sunny suburbs — your FICO score may be the single most powerful number standing between you and the keys to your new home. Understanding how it works and what resources exist to strengthen it, is essential knowledge for every prospective buyer.

What Is a FICO Score?

A FICO score is a three-digit credit score calculated by the Fair Isaac Corporation, ranging from 300 to 850. Mortgage lenders across Utah use this number to assess lending risk — in other words, how likely you are to repay a home loan on time. The higher your score, the more favorable the terms lenders will offer.

Your FICO score is calculated from five key factors:

- Payment History (35%) — The biggest factor. On-time payments build your score; late payments damage it.

- Amounts Owed / Credit Utilization (30%) How much of your available credit you’re using. Keep the balance below 30%.

- Length of Credit History (15%) Older accounts demonstrate long-term reliability.

- Credit Mix (10%) Having a variety of credit types (cards, auto loans, mortgages) helps.

- New Credit Inquiries (10%). Too many recent applications can temporarily lower your score.

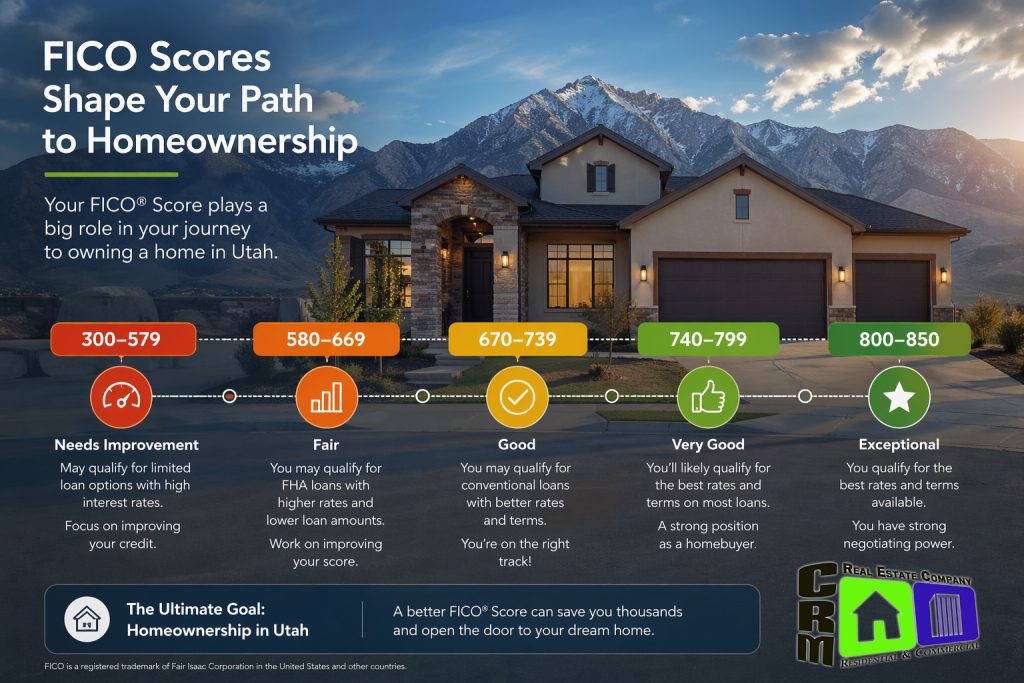

FICO Score Ranges at a Glance

How FICO Scores Affect Your Ability to Buy

Your credit score touches nearly every aspect of the mortgage process — from whether you qualify at all, to the interest rate you’re offered, and even the size of the down payment required. Here’s how the numbers break down in real terms for Utah home buyers:

| FICO Score | Rate Tier | Typical Impact |

| 760 and above | Best Available | Lowest interest rates, best loan terms |

| 700 – 759 | Good | Competitive rates, most programs available |

| 640 – 699 | Fair | Higher rates, fewer loan options |

| 580 – 639 | Below Average | FHA only, higher costs, PMI required |

| Below 580 | Poor | Very limited options, may need credit repair first |

Consider this: the difference between a 620 and a 760 FICO score on a $450,000 Utah home loan could mean baying $200-$400 more per month – adding up to tens of thousands of dollars over the life of a 30-year mortgage. Even a modest score improvement can translate directly into real savings.

Beyond interest rates, your FICO score also determines which loan programs you’re eligible for. Conventional loans typically require a minimum score of 620. FHA loans may accept scores as low as 580 with a 3.5% down payment, or even 500–579 with 10% down. VA and USDA loans have more flexible credit requirements, but still conduct underwriting reviews.

Programs to Help Utah Buyers Improve Their FICO Score

The good news: a poor credit score is not a permanent barrier. Utah offers a strong ecosystem of programs — at the federal, state, and nonprofit level — designed to help buyers repair credit, build financial literacy, and reach homeownership readiness.